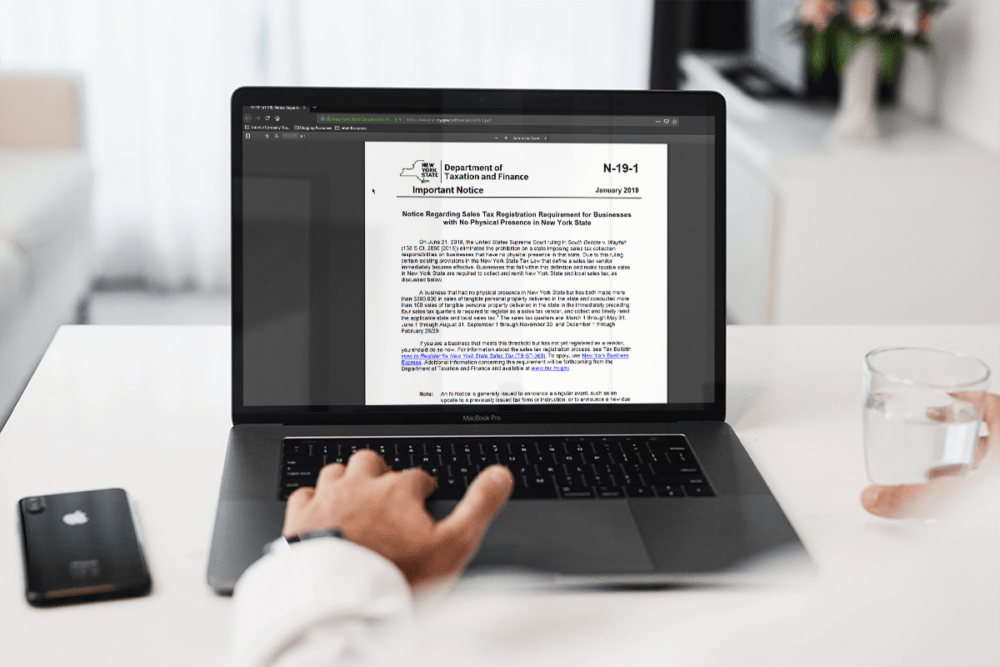

From our friends at Avalara: The New York State Department of Taxation and Finance announced that due to the South Dakota v. Wayfair Supreme Court ruling last year, an existing provision in New York Sales Tax Law defining a sales tax vendor became immediately effective. Any business within this definition making taxable sales into the state is required to be registered as a New York State vendor and to collect & remit sales tax. This can impact your clients and they should know.

Talk to An Advisor Today

You might also like these articles

Year End Accounting Checklist for Financial Success

Read More

Year End Accounting Checklist: How To Close the Fiscal Year Year end is here, and it’s time to get your QuickBooks year end accounting checklist ready! While it may seem like it came out of nowhere, it’s important to be prepared. Many businesses find themselves overwhelmed with financial tasks and time management when closing the…

Choose QuickBooks Enterprise or Advanced

Read More

As businesses grow and evolve, their needs change. One ongoing challenging decision is selecting the right accounting system. Numerous factors come into play, including readiness for upgrades or switches, and determining the most suitable configuration for your industry. To help you decide what would be the best fit for your business, we will be comparing…

Milestones to Skyrocketing Growth: Celebrating A Remarkable Year

Read More

In a dynamic business landscape where only the most adaptable thrive, our journey over the past year has been nothing short of spectacular. Charting a trajectory marked by strategic acquisitions and fueled by relentless dedication, Out of the Box Technology has not only expanded its footprint but also proudly clinched a coveted spot on the…

Out of the Box Technology is on the Inc. 5000 List!

Read More

For the 5th time, we are excited to share the news that Out Of The Box Technology has made the Inc. 5000 list this year! This award recognizes the fastest-growing companies in America, many of which have grown six-fold since 2016 alone. Not only have the companies on the 2021 Inc. 5000 been very competitive within their markets, but…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

April 15, 2024

Choose QuickBooks Enterprise or Advanced

Business Software & Apps, Free Resources, News & Resources, QuickBooks, QuickBooks Desktop, QuickBooks Online, Recent News, Tips & Tricks

We recommend QuickBooks because we:

- Know its vast array of functional capabilities, and

- Understand its high flexibility in accommodating wide ranges of varying solution configurations.

This allows us to design a custom-tailored solution to meet and exceed your business needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

June 30, 2025

Bookkeeping for Big Purchases

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful)

Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries.

And here’s the catch: If you don’t book these purchases correctly, your financials can quickly become inaccurate.

Poorly tracked equipment purchases can lead to:

-

Misstated profit and loss reports

-

Inaccurate cash flow projections

-

IRS audits or tax issues

-

Missed deductions on depreciation

-

Confusion between asset value and loan balances

In this guide, we break down how to track equipment financing the right way using proper bookkeeping methods. Whether you’re using QuickBooks, Xero, or another accounting platform, this article will help you ensure your books reflect the real financial picture.

Table of Contents

-

Why Equipment Financing Is Harder Than It Looks

-

Key Accounts You Need to Set Up

-

How to Book a Financed Equipment Purchase (Step-by-Step)

-

Example: Booking a $50,000 Truck Purchase

-

How to Track Equipment Loans and Payments

-

Depreciation: What You Must Know

-

Tax Considerations for Financed Equipment

-

How to Automate and Stay Audit-Ready

-

FAQs

-

Final Thoughts

1. Why Equipment Financing Is Harder Than It Looks

When you finance equipment, you’re not just making a purchase—you’re entering into a long-term liability that spans multiple years and affects cash flow, tax deductions, and asset values. Yet many business owners make one of these mistakes:

-

Booking the entire purchase price as an expense

→ This inflates expenses and understates profits -

Not tracking the loan separately

→ This makes it unclear what’s still owed vs. what’s owned -

Ignoring depreciation

→ You may miss tax benefits or violate accounting standards -

Using the wrong expense category

→ Leads to confusion in financial reports or misalignment with your CPA

A study from the National Federation of Independent Business (NFIB) found that nearly 40% of small business owners lack clear guidance on booking capital equipment, especially if purchased via financing.

2. Key Accounts You Need to Set Up

Before you make the purchase, your chart of accounts should include:

| Account Name | Type | Purpose |

|---|---|---|

| Equipment or Machinery | Fixed Asset | Records the value of the purchased item |

| Equipment Loan | Long-Term Liability | Tracks the financing owed to the lender |

| Interest Expense | Expense | Separates interest payments from principal |

| Depreciation Expense | Expense | Tracks yearly depreciation |

| Accumulated Depreciation | Contra Asset | Offsets asset value over time |

| Loan Payable – Current | Current Liability | Reflects the portion due in the next 12 months |

You can add these accounts manually or consult your bookkeeper or accountant to set them up accurately in QuickBooks or other software.

3. How to Book a Financed Equipment Purchase (Step-by-Step)

Here’s a simplified, step-by-step guide:

Step 1: Record the Full Equipment Purchase

Even if you didn’t pay in full, book the total cost of the equipment as a fixed asset.

-

Debit: Equipment (Asset) → $50,000

-

Credit: Equipment Loan (Liability) → $50,000

Step 2: Record the Down Payment (If Any)

-

Debit: Equipment Loan → $10,000

-

Credit: Bank or Cash → $10,000

Now your liability reflects the remaining amount financed.

Step 3: Record Monthly Loan Payments

Each monthly payment includes principal + interest. Split it like this:

-

Debit: Equipment Loan → $800 (principal portion)

-

Debit: Interest Expense → $200 (interest portion)

-

Credit: Bank → $1,000 (total payment)

Step 4: Record Depreciation Monthly or Annually

-

Debit: Depreciation Expense → $833.33

-

Credit: Accumulated Depreciation → $833.33

(Based on a 5-year straight-line depreciation schedule for $50,000)

4. Example: Booking a $50,000 Truck Purchase

Let’s say you buy a $50,000 service truck with:

-

$10,000 down

-

$40,000 financed over 5 years at 6% interest

Initial Entry:

-

Equipment (Asset) → $50,000

-

Equipment Loan (Liability) → $50,000

Down Payment:

-

Debit: Loan → $10,000

-

Credit: Bank → $10,000

Monthly Payment ($773):

-

$640 is principal

-

$133 is interest

-

Debit Loan → $640

-

Debit Interest Expense → $133

-

Credit Bank → $773

Depreciation (Straight Line over 5 years):

-

Annual: $10,000

-

Monthly: $833.33

-

Debit Depreciation Expense → $833.33

-

Credit Accumulated Depreciation → $833.33

5. How to Track Equipment Loans and Payments

Use a Loan Amortization Schedule

This shows each payment’s breakdown between interest and principal. You can generate one in Excel or use accounting software tools.

Reconcile Monthly

Match actual payments to your schedule. Adjust for fees, prepayments, or skipped payments.

Monitor Interest Expense

Keep interest separate from the asset value—it’s a cost of borrowing, not an investment.

6. Depreciation: What You Must Know

Depreciation spreads the cost of an asset over its useful life, giving you a tax deduction each year instead of all at once.

Common Depreciation Methods:

-

Straight Line: Equal amount each year

-

MACRS (Modified Accelerated Cost Recovery System): IRS-approved accelerated method

-

Section 179: Deduct up to $1,220,000 of eligible equipment purchases in 2024

IRS Equipment Life Categories:

-

Vehicles: 5 years

-

Computers: 5 years

-

Office furniture: 7 years

-

Heavy equipment: 7–10 years

Accumulated Depreciation

This is a contra-asset account that reduces the equipment’s book value over time. On your balance sheet:

-

Equipment = $50,000

-

Accumulated Depreciation = –$20,000

-

Net Equipment Value = $30,000

7. Tax Considerations for Financed Equipment

Section 179 Deduction

You can write off the full purchase price (not just what you paid out-of-pocket) in the year the equipment is put into service.

Bonus Depreciation

Allows 60% deduction for eligible property placed in service during the tax year, on top of Section 179.

Interest Deductibility

Business loan interest is tax-deductible—track it separately from the principal to maximize this deduction.

8. How to Automate and Stay Audit-Ready

Use Cloud-Based Bookkeeping Tools

QuickBooks Online, Xero, and Zoho Books all support fixed asset tracking, loan schedules, and depreciation automation.

Document Everything

Store invoices, financing agreements, amortization schedules, and depreciation reports digitally. Keep them organized by asset.

Create Reports Quarterly

Run your balance sheet and profit & loss statement quarterly to check for accuracy. Look for:

-

Equipment showing on balance sheet

-

Loan balance reducing over time

-

Interest showing as an expense

-

Depreciation posting consistently

Work with a Pro

Even if you manage your books internally, consult with a bookkeeping expert or CPA annually to ensure compliance.

9. FAQs

Can I record a financed equipment purchase as an expense?

No. It must be recorded as a fixed asset, not a direct expense. Only depreciation and interest count as expenses over time.

What happens if I trade in old equipment?

You’ll need to remove the old asset from your books and calculate gain/loss on the trade-in. This affects both asset and liability accounts.

Can I use Section 179 if I didn’t pay in full?

Yes. Even if you financed the equipment, you may still deduct the full cost—assuming you meet eligibility requirements and placed the asset in service during the tax year.

Should I record sales tax in the asset cost?

Yes. Include sales tax, shipping, and setup fees in the total asset cost to be depreciated.

What if I pay off the loan early?

Update your loan balance and amortization schedule accordingly. You may save interest, but still need to track the full equipment value.

10. Final Thoughts

Equipment financing can help you scale your business, but it brings complexity to your bookkeeping. By setting up the right accounts, accurately tracking loans, properly depreciating assets, and following IRS rules, you’ll keep your financials clean—and your CPA happy.

Avoid shortcuts. Improper booking can lead to audit flags, misstated earnings, and missed deductions. Instead, follow this structured approach or partner with a professional to ensure your books reflect the true value of your business assets.

Need Help With Bookkeeping for Equipment Financing?

Out of the Box Technology specializes in helping businesses track big purchases the right way. From QuickBooks setup to depreciation tracking, we’ll help you stay compliant, tax-optimized, and audit-ready.

Ready to Improve Your Bookkeeping?

Out of the Box Technology helps contractors implement job costing with QuickBooks and other platforms. Whether you’re just getting started or ready to automate job-level reporting, our experts can guide you every step of the way.

Learn more about our services at [Link to Out of the Box Technology Services Page].

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

The Complete Guide to Data Migration for Pest Control Businesses

Read More

Why Pest Control Needs Data Migration Pest control companies handle a large amount of critical data—customer contact records, treatment schedules, chemical logs, compliance documentation, jobsite photos, invoices, technician notes, and more. Many businesses begin by storing this information in spreadsheets or on paper. But as the business grows, these systems become inefficient and error-prone. Data…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

June 27, 2025

The Complete Guide to Data Migration for Pest Control Businesses

Why Pest Control Needs Data Migration

Pest control companies handle a large amount of critical data—customer contact records, treatment schedules, chemical logs, compliance documentation, jobsite photos, invoices, technician notes, and more. Many businesses begin by storing this information in spreadsheets or on paper. But as the business grows, these systems become inefficient and error-prone.

Data migration is the process of transferring this information into a new, more capable platform—typically a cloud-based CRM or pest control software solution. It’s not just about moving data; it’s about unlocking better business performance.

When executed properly, data migration helps pest control businesses:

-

Streamline technician workflows

-

Automate regulatory compliance

-

Improve customer experience

-

Eliminate double data entry

-

Enable future growth with scalable systems

But without a proper plan, data migration can be risky—leading to lost information, downtime, or system mismatches. This guide walks through the full migration process for pest control companies, offering step-by-step instructions, real-world scenarios, and frequently asked questions to help you migrate confidently.

Why Pest Control Companies Should Migrate Data

1. Stay Compliant

Many states and localities require pest control businesses to maintain detailed records of treatments, chemicals used, technician certifications, and site visits. Paper systems or legacy software often fall short, putting companies at risk during audits. Data migration to a digital system makes documentation fast, reliable, and accessible.

2. Consolidate Disconnected Systems

It’s common for pest control businesses to use different platforms for customer contacts, scheduling, invoices, and compliance. This leads to disconnected data and inefficient operations. Migrating to a single system—or integrating multiple systems—creates a central source of truth.

3. Boost Productivity

When technicians can see job history, treatment records, and notes from their phones in the field, they complete jobs faster and with fewer errors. Office staff also spend less time looking up records, making phone calls, or entering the same data multiple times.

4. Prepare for Growth

Whether you’re adding new team members, expanding into new service areas, or acquiring other businesses, a modern system makes onboarding and expansion easier. Data migration ensures your foundational systems are strong enough to support future growth.

Common Data Sources to Migrate

Here are the most common types of data involved in a pest control migration:

| Data Type | Common Sources |

|---|---|

| Customer & contact records | Spreadsheets, paper forms, CRMs |

| Job history & treatments | Logbooks, field service apps |

| Schedules & dispatch info | Paper calendars, job boards, scheduling tools |

| Invoices & billing | QuickBooks, spreadsheets, payment apps |

| Chemical usage records | Paper logs, Excel, compliance software |

| Jobsite photos | Google Drive, Dropbox, technician devices |

| Technician timesheets | Spreadsheets, time-tracking tools |

| Equipment logs | Manual logs, inventory spreadsheets |

Why Data Migrations Fail (and How to Prevent It)

Data migration is not just a technical task—it’s a strategic one. When done without preparation, it can fail due to:

-

Lack of a detailed plan

-

Poor data hygiene (duplicates, errors)

-

Misaligned data fields across systems

-

No testing phase

-

Inadequate staff training

The key to avoiding failure is following a structured, phased approach.

The 5 Phases of Data Migration for Pest Control Businesses

Phase 1: Planning and Assessment

-

Inventory your data: Identify what systems you’re currently using and what data needs to be moved.

-

Set clear goals: Decide what success looks like. Will you migrate everything or just recent years of records?

-

Assemble your migration team: Include office staff, field managers, compliance leads, and your software vendor or migration partner.

-

Schedule wisely: Plan to migrate during your slow season to reduce disruption.

Phase 2: Backup and Security

-

Create full backups of all data before migration.

-

Use secure storage and encrypted transfers.

-

Limit access to sensitive information to authorized team members only.

Phase 3: Data Mapping and Cleansing

-

Map data fields: Align the fields from your old system with those in the new one. Example: “Service Date” in a spreadsheet becomes “Job Completed Date” in the new system.

-

Clean your data: Remove duplicates, fill in missing fields, and standardize formats (such as address and phone number formats).

-

Prepare files: Format spreadsheets or exports according to your new software’s import guidelines.

Phase 4: Testing and Validation

-

Perform a test migration using a small sample of data.

-

Check for errors, mismatches, and missing information.

-

Get feedback from field technicians and office staff.

-

Make necessary adjustments before proceeding with the full migration.

Phase 5: Full Migration and Go-Live

-

Migrate data in logical phases: start with customer data, then jobs, invoices, chemical records, and finally media files like photos.

-

Provide training to your team to ensure they know how to use the new system.

-

Keep your old system read-only for a few months post-migration in case you need to verify historical data.

Real-World Example: A Pest Control Company’s Migration

A 10-technician pest control company had been using a mix of spreadsheets, QuickBooks Desktop, and physical treatment logs. They migrated to a cloud-based field service platform with the following results:

-

Migration Timeframe: 5 weeks (including testing and training)

-

Data Migrated: 3,200 customer records, 5 years of job history, 1,100 chemical treatment records, and 2,000 photos

-

Impact:

-

Reduced admin workload by 25%

-

Eliminated duplicate customer records

-

Cut invoicing time from 3 days to 3 hours per month

-

Improved audit preparedness with digital treatment logs

-

Common Challenges and Solutions

| Challenge | Solution |

|---|---|

| Duplicate or outdated customer data | Use deduplication tools and review records before import |

| Missing or inconsistent field formats | Standardize formats (e.g., date formats, phone numbers) |

| Technicians unsure how to access new data | Provide hands-on training and quick-reference guides |

| Large volumes of attachments and photos | Compress and batch-upload photos tied to job IDs |

| Regulatory fields not mapping correctly | Work with your software provider to customize field mapping |

Benefits of a Successful Data Migration

-

✅ Better visibility into operations with centralized dashboards

-

✅ Faster scheduling and dispatch using real-time data

-

✅ Compliance readiness with digital logs and chemical records

-

✅ Improved customer service through faster response and access to job history

-

✅ Higher efficiency by reducing duplicate entries and manual work

-

✅ Scalability for adding new staff or locations

FAQs

Q: How long does a data migration take?

A typical migration takes 4–6 weeks, including planning, testing, and training. More complex migrations may take longer.

Q: Will I lose my job history or photos?

Not if the data is properly backed up and mapped. Testing is key to preserving job records and media files.

Q: Can I do the migration myself?

Some businesses handle basic migrations in-house. However, if your data is stored in multiple systems or includes regulatory logs, it’s best to work with an expert.

Q: Will migration disrupt our daily operations?

It shouldn’t, if planned well. Most businesses migrate during slower months and continue using their old system until the new one is ready to go live.

Q: What if some data doesn’t fit into the new system?

Most platforms offer custom fields or import tools. You may also work with a consultant to configure the system to your needs.

Conclusion: Migrate with Confidence

Pest control businesses rely on data for scheduling, compliance, customer service, and growth. Migrating to a more modern, integrated system is one of the smartest investments you can make.

With proper planning, secure backups, thorough testing, and team training, you can avoid the most common migration pitfalls and come out stronger on the other side. Whether you’re moving off spreadsheets, retiring legacy software, or combining systems after an acquisition, a structured data migration ensures your business is ready for what’s next.

Want Help with Your Data Migration?

Out of the Box Technology specializes in helping pest control businesses migrate confidently. From QuickBooks to CRM to compliance data, we’ll handle the hard part—so you can get back to doing what you do best.

Schedule Your Free Consultation

We’ll handle the migration so you can get back to doing what you do best: running your business.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.