The software is ready. The question is whether your implementation will be.

Here is a tension worth naming at the start: Intuit Enterprise Suite is one of the most credible mid-market ERP platforms to arrive in a generation: cloud-native, AI-powered, multi-entity, and built on a QuickBooks foundation that most finance teams already know. And yet, ERP implementations still fail to meet their original objectives at a rate of 55–75%, depending on who’s measuring. Gartner puts the figure at roughly 70%.

Software did not create that gap. Implementation did.

The variable that decides which side of that statistic your organization lands on is not the product you buy. It is the partner you choose to implement it.

Intuit Enterprise Suite Has Changed the Mid-Market ERP Equation

For the better part of two decades, mid-market finance teams faced a genuine “missing middle” problem. QuickBooks was too thin for a multi-entity business running real complexity. NetSuite and Sage Intacct delivered real power, but also 12-month implementation timelines, six-figure consulting fees, and a steep adoption curve that often erased whatever efficiency gains were promised.

What IES actually delivers

Intuit Enterprise Suite, launched in September 2024, was built specifically to fill that gap. It is cloud-native, AI-native, and designed for businesses that have genuinely outgrown QuickBooks Online Advanced: multi-entity consolidation, dimensional reporting, project-level job costing, integrated payroll and HR, and an AI agent layer that handles reconciliation, bank feed categorization, and expense allocation.

A commissioned Forrester study projects up to 299% ROI over three years for IES customers. The February 2026 launch of the Intuit ENt Construction Edition, Intuit’s first industry-specific ERP vertical, and the Spring 2026 release wave (multi-entity close automation, dimensional reporting enhancements, expanded HCM capabilities) signal that Intuit is investing aggressively in the platform.

Why this matters now

The “missing middle” finally has a real option. For a $20M construction company, a PE-backed home services platform, or a founder-led business running three QuickBooks files and a folder full of Excel consolidations, Intuit Enterprise Suite is no longer a compromise , it is a genuine upgrade path.

Intuit reports that 95% of Intuit Enterprise Suite customers complete migration in under 30 days. That is a meaningful number. It is also a floor, not a ceiling, and the distinction matters more than most buyers realize.

But the Software Alone Doesn’t Guarantee the Outcome

Speed without design quality is technical debt deferred, not value created.

The three causes of ERP implementation failure, consistently identified across Panorama Consulting’s annual research, are: inadequate organizational change management, poor data quality and migration, and inexperienced implementation teams. All three are fully within a partner’s control. None of them are software problems.

For most mid-market buyers, the picture is familiar:

- Years of QuickBooks workarounds have created duplicate vendors, misclassified chart of accounts entries, and stale balances. Migration surfaces every shortcut ever taken.

- The finance team is running the close; they are not learning a new ERP on the side.

- IES is new enough that experienced practitioners are genuinely scarce. An ERP partner with NetSuite or Sage Intacct certifications is not automatically qualified for IES.

- Multi-entity complexity, PE rollup structures, and integration sprawl (payroll, AP automation, sales tax, field-service platforms) mean the ERP is only as good as the architecture around it.

A technically clean go-live that hasn’t addressed any of those realities is not a success. It is a setup for a second engagement.

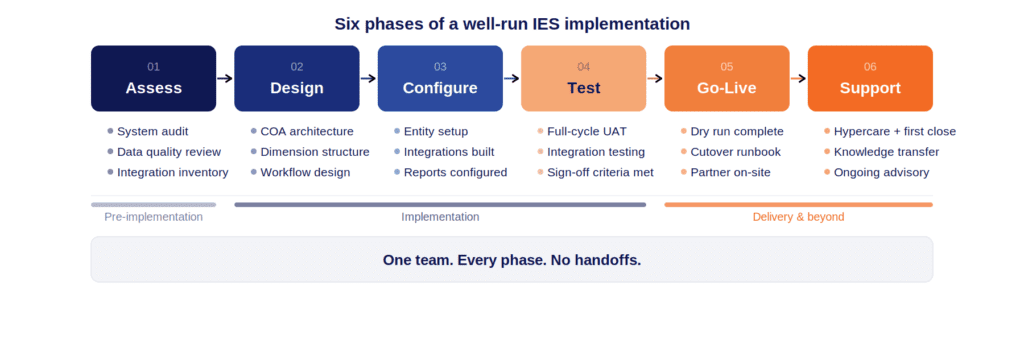

The Six Phases of a Well-Run Intuit Enterprise Suite Implementation

A successful implementation is not a single project with a go-live date. It is a sequence, and the same team should carry it from start to finish.

What a True Implementation Partner Does Differently

There is a meaningful difference between a partner who configures a system and a partner who designs one. The difference shows up at your first quarterly close.

1. Design before configuration

The chart of accounts, dimension structure, entity hierarchy, and reporting model should be architected before anyone touches the system. A well-designed COA built around how your business actually operates (by project, location, department, and entity) makes every future report, audit, and acquisition integration dramatically easier. The reverse approach, configuring first and fitting the business to the system later, is the most common implementation failure mode.

2. Field-level integration, not “connectors that work”

“The integration works” is not the same as “the data is trustworthy.” A serious integration engagement maps field-by-field, tests edge cases (partial shipments, credit memos, multi-entity intercompany transactions), and validates outputs against known results before the system is live. Connectors that pass end-to-end testing in isolation often break in production when real transaction volume hits unusual paths.

3. Full-cycle user acceptance testing

Testing features is not the same as testing your business. A full UAT engagement runs order-to-cash and procure-to-pay as complete cycles, from the first touchpoint to the financial statement. It surfaces the gaps between what the system does and what your team actually does, before those gaps become month-end surprises.

4. A cutover runbook with assigned owners

The go-live weekend should be the most boring weekend of the project. That requires a step-by-step cutover runbook: dry runs completed, tasks assigned by name (not by role), parallel processing logic defined, rollback criteria documented. The organizations that experience dramatic go-lives are usually the ones that skipped the dry run.

5. Hypercare that earns the name

Hypercare is not a ticketing queue. Real hypercare means daily standups in the first two weeks, explicit support through the first month-end close, and a formal knowledge transfer process before the engagement winds down. The first close on a new system is when the gaps between training and reality become visible. A partner who is present for that close has a fundamentally different relationship with the outcome than one who hands over documentation and opens a support ticket portal.

6. AI agent configuration

Intuit Enterprise Suite Accounting, Payments, Finance, and Project Management agents are genuinely capable, but they require workflow-specific configuration to deliver value. Default agent settings are generic. A partner who understands how your business actually processes invoices, expenses, and bank feeds can configure agents to return real hours to your finance team. This is increasingly the differentiator as the IES agent surface area expands.

The Six Phases of a Well-Run Intuit Enterprise Suite Implementation

A successful implementation is not a single project with a go-live date. It is a sequence — and the same team should carry it from start to finish.

Assess — Current system audit, data quality review, integration inventory, and entity mapping. The output is a clear picture of where you are and what the migration will require. Surprises here are features, not bugs: a thorough assessment prevents worse surprises later.

Design — COA architecture, dimension structure, reporting model, workflow design, and integration specifications are documented before any configuration begins. The Configuration Design Document produced here is the reference point for every subsequent decision.

Configure — System build against the approved design. Entity structure, user roles, permissions, workflow rules, integration connections, and custom report templates.

Test — Full-cycle UAT against real business scenarios. Integration testing end-to-end. Performance validation. Issue log and resolution. Sign-off criteria met before proceeding.

Go-Live — Dry run completed. Cutover runbook executed. Parallel processing managed. Your team is running live on IES with dedicated partner support present.

Support — Hypercare through the first close. Formal knowledge transfer. Transition to ongoing advisory or controller/CFO-level support as needed.

No handoffs between phases. No sales-to-delivery-to-support relay races. One team, every step.

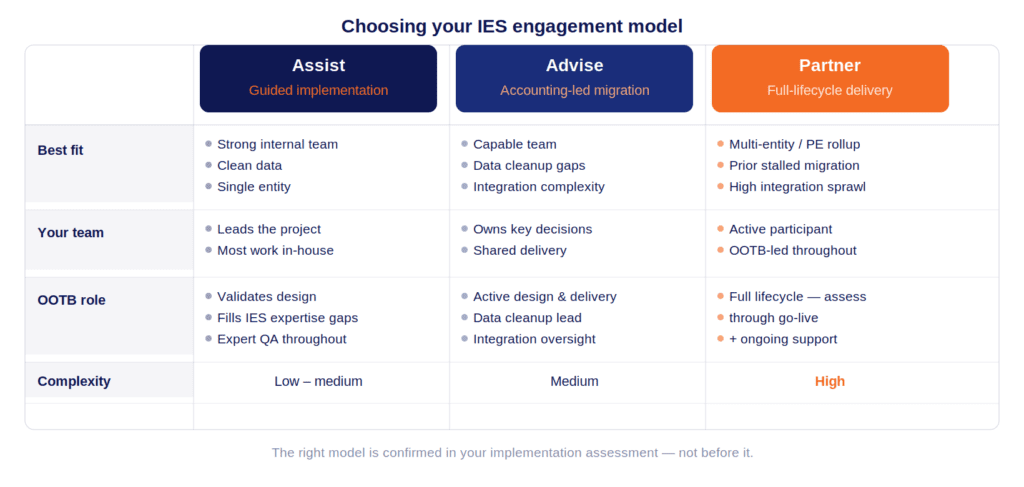

Choosing the Right Engagement Model for Your Situation

Not every Intuit Enterprise Suite migration is the same complexity — and the right engagement model depends on what you are bringing to the table.

Industry Matters: Why a Specialist Beats a Generalist

A general-purpose ERP implementer can configure a chart of accounts. They cannot necessarily design one for a construction contractor that needs certified payroll, WIP reporting against percentage-of-completion, AIA-style billing, job cost variance analysis, and retention tracking.

Construction — IES now includes the Construction Edition, with dedicated job costing, WIP reporting, AIA invoicing, and an AI-powered Project Management Agent. Implementing it correctly requires understanding the accounting — how costs flow from labor and equipment to job cost codes, how WIP schedules are produced, how over/under billings are recognized. An implementation partner who has served contractors knows this before the first design meeting.

Home and commercial services — Field-service-to-accounting integration is where margin visibility lives or dies for a services business. Technician-level profitability, dispatch-to-invoice reconciliation, fleet cost allocation — these are accounting design questions, not just technical integration questions. Intuit Enterprise Suite’s project management and job costing capabilities are purpose-built for this, but only if they are configured by someone who understands how a services business actually operates.

Private equity and multi-entity portfolios — The value of IES for a PE portfolio company or roll-up is consolidated reporting on demand, a standardized COA across entities, and the ability to absorb a new acquisition without rebuilding the finance stack. Delivering that requires intercompany elimination account design, dimension standardization across entities, and investor-grade reporting templates built from day one. Read how Intuit Enterprise Suite enables multi-entity consolidation here.

How to Evaluate an Intuit Enterprise Suite Implementation Partner: A Buyer’s Checklist

Before you select a partner, these are the questions worth asking, and pressing on if the answers are vague.

On design and methodology

- Do they design the COA and dimension architecture before configuration begins — or do they configure and adapt?

- Can they show you a sanitized Configuration Design Document from a prior engagement?

- What does their cutover runbook look like? Can they walk you through a real example?

On expertise and continuity

- Who is the named advisor on this engagement, and is that person delivering, not just selling?

- Do they have IES-specific implementation experience, or are they treating it like a prior ERP they know better?

- Do they have accounting expertise in-house, or primarily systems integration?

On hypercare and post-go-live

- What does hypercare include, specifically? Daily standups? First-close support? Or a support ticket queue?

- Can they provide controller- or CFO-level advisory support after go-live if your needs evolve?

On industry and references

- Do they have clients in your specific industry, not just finance clients generally?

- Can they provide references willing to speak about the first close after go-live?

The answers to these questions separate partners who have done this from partners who will use your implementation to learn.

The Real Measure of Success

Go-live is not success. Go-live is the beginning of the real work.

The genuine measures of a successful Intuit Enterprise Suite implementation show up later: the first quarterly close that runs in five days instead of fifteen. The first audit where the finance package comes out of the system rather than being reconstructed for auditors. The first lender reporting package that goes out on day three of the month. The first acquisition where the new entity is consolidated within weeks, not quarters.

Intuit Enterprise Suite creates the conditions for those outcomes. A skilled implementation partner closes the gap between the software’s potential and your organization’s reality.

The organizations that experience a stalled migration, a costly second engagement, or a system the finance team doesn’t trust, almost always made the same mistake: they treated implementation as a technical problem when it is actually an accounting and organizational design problem.

Choose the partner who optimizes for your first clean close, not for the shortest possible go-live date.

Ready to Assess Your Intuit Enterprise Suite Implementation?

Out of the Box Technology has completed 25,000+ migrations across QuickBooks Desktop, QBO Advanced, NetSuite, Sage, Dynamics, and SAP — with a team of 60+ US-based professionals and 35+ years in business. Our Intuit Enterprise Suite engagements are led by accounting professionals, not systems integrators.

Schedule a 30-minute Intuit Enterprise Suite Implementation Assessment.

One conversation, no obligation. We’ll review your current system, data quality, and integration landscape and tell you honestly which engagement model fits, or whether there’s preparation work to do first. A written proposal with scope, timeline, and fees follows within one week.

Related reading:

Frequently asked questions