One of the many challenges businesses need to stay ahead of is cyber security. Many service providers and their products have added stricter requirements during the account creation and product acquisition stages. However, there are still service providers not having adapted their requirements to growing trends in Internet Security.

Talk to An Advisor Today

You might also like these articles

How to Plan a Data Migration in 6 Easy Steps

Read More

If you’re preparing to switch systems, upgrade software, or clean up years of financial history, you may be facing one of the most crucial IT processes: data migration. For QuickBooks users, this often means replacing a company data file to fix performance issues, eliminate errors, or transition to a newer version of QuickBooks. Whether you’re…

6 Key Reasons Why Keeping Your Bookkeeping Updated Matters

In today’s fast-paced business world, maintaining accurate and up-to-date financial records is crucial for long-term success. Whether you're a small business owner, a franchise operator, or managing a growing enterprise, bookkeeping updates should never be overlooked. Outdated bookkeeping can lead to cash flow issues, tax penalties, and even legal troubles. On the other hand, businesses...

Read More

Controller vs. Comptroller: Key Differences Explained for Home Service Business Owners

Understanding the Differences Between a Controller and a Comptroller When running a home service business—whether it’s plumbing, HVAC, roofing, or landscaping—financial management plays a crucial role in your success. As your business grows, you may need to hire a financial professional to oversee your finances and ensure financial stability. But should you hire a Controller...

Read More

Essential Small Business Bookkeeping Resources: Your Go-To Hub

Bookkeeping is the foundation of any successful small business. Keeping track of financial transactions, expenses, and revenue ensures that businesses remain profitable, compliant, and financially healthy. However, many small business owners struggle to manage their bookkeeping efficiently due to time constraints, lack of expertise, or limited resources. In this guide, we’ll explore essential small business...

Read More

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

February 24, 2025

6 Key Reasons Why Keeping Your Bookkeeping Updated Matters

In today’s fast-paced business world, maintaining accurate and up-to-date financial records is crucial for long-term success. Whether you’re a small business owner, a franchise operator, or managing a growing enterprise, bookkeeping updates should never be overlooked.

Outdated bookkeeping can lead to cash flow issues, tax penalties, and even legal troubles. On the other hand, businesses that prioritize bookkeeping services gain better financial clarity, improved decision-making, and streamlined operations.

In this article, we’ll explore the six key reasons why keeping your bookkeeping updated matters and how it can impact your business’s financial health.

1. Accurate Financial Reporting and Decision-Making

Why It Matters

Your financial reports provide a real-time snapshot of your business’s financial health. Outdated or inaccurate bookkeeping can lead to poor decision-making, impacting cash flow, profitability, and long-term growth.

Data-Backed Insight

According to a Small Business Administration (SBA) report, 82% of businesses fail due to cash flow mismanagement. Keeping your books updated ensures you always have a clear picture of your revenue, expenses, and profitability.

How Bookkeeping Updates Help

✅ Generate accurate profit and loss statements

✅ Track monthly revenue vs. expenses

✅ Identify profit margins and growth trends

✅ Make data-driven business decisions

Example

Imagine running a plumbing business and not realizing that material costs have increased by 15% over the last six months. Without updated bookkeeping, you might continue to price services based on outdated costs, reducing profitability.

2. Ensures Compliance with Tax Regulations

Why It Matters

Tax compliance is a legal obligation for all businesses. Late or incorrect tax filings can lead to heavy penalties, audits, or legal consequences.

Data-Backed Insight

According to the IRS, 40% of small businesses incur an average of $845 per year in tax penalties due to incorrect filings.

How Bookkeeping Services Help

✅ Keep track of tax-deductible expenses

✅ Ensure on-time tax filings

✅ Prevent penalties for late payments

✅ Prepare audit-proof financial records

Example

If you’re a franchise owner running multiple locations, missing even a single tax deadline can lead to compounded penalties. With regular bookkeeping updates, your accountant can file returns accurately and on time.

3. Improved Cash Flow Management

Why It Matters

Many businesses struggle with cash flow problems due to untracked receivables and unexpected expenses. Without accurate bookkeeping, you risk running out of cash when you need it the most.

Data-Backed Insight

A study by U.S. Bank found that 82% of small business failures are due to poor cash flow management.

How Bookkeeping Updates Help

✅ Track accounts receivable and payable

✅ Identify slow-paying customers

✅ Forecast seasonal fluctuations

✅ Avoid late fees and overdraft charges

Example

A home services business (e.g., HVAC repair) might experience seasonal revenue fluctuations. Without updated bookkeeping, the owner might overspend in peak months and struggle to cover payroll during slower months.

4. Better Business Growth and Financial Planning

Why It Matters

Without accurate financial records, planning for growth becomes challenging. Whether you’re seeking a business loan, expanding locations, or hiring staff, lenders and investors need up-to-date financials before approving funding.

Data-Backed Insight

According to a study by Nav, 82% of small businesses that applied for loans were denied due to poor financial documentation.

How Bookkeeping Services Help

✅ Ensure clean financial records for loan approvals

✅ Identify profitable service lines

✅ Forecast business expansion opportunities

✅ Secure better investor confidence

Example

A growing bookkeeping franchise looking to open a new location must present accurate financial records to secure a business loan. Without updated books, securing funding becomes nearly impossible.

5. Detects and Prevents Fraud or Financial Errors

Why It Matters

Fraud and accounting errors can drain business profits without immediate detection. Regular bookkeeping updates help identify suspicious transactions and prevent financial mismanagement.

Data-Backed Insight

The Association of Certified Fraud Examiners (ACFE) reports that businesses lose 5% of annual revenue due to fraud, with small businesses being the most vulnerable.

How Bookkeeping Updates Help

✅ Detect unauthorized transactions

✅ Identify accounting errors before they escalate

✅ Reduce theft and mismanagement risks

✅ Ensure reconciled bank statements

Example

A landscaping business with multiple employees might find discrepancies in vendor payments. Regular bookkeeping audits can flag duplicated or fraudulent invoices before they cause significant losses.

6. Saves Time and Reduces Stress for Business Owners

Why It Matters

Bookkeeping is time-consuming, especially for business owners managing operations, sales, and customer service. Outsourcing bookkeeping services or keeping records updated saves hours of manual work and reduces financial stress.

Data-Backed Insight

A study by Clutch found that 45% of small business owners spend more than 80 hours per year on bookkeeping and taxes.

How Bookkeeping Services Help

✅ Free up valuable time for business operations

✅ Avoid last-minute tax season stress

✅ Reduce manual data entry errors

✅ Improve overall work-life balance

Example

A roofing contractor handling both client projects and bookkeeping may struggle to keep up with financial records. Outsourcing bookkeeping saves time and allows them to focus on growing their business.

FAQs

1. How often should I update my bookkeeping records?

It’s recommended to update your bookkeeping weekly or monthly to ensure accurate financial tracking.

2. Can I manage bookkeeping myself, or should I hire a service?

While small businesses can use software like QuickBooks or Xero, outsourcing bookkeeping services ensures accuracy and compliance.

3. How much does bookkeeping cost for small businesses?

The cost varies based on business size and complexity. Outsourced bookkeeping services range from $300 to $2,500 per month.

4. What happens if I don’t keep my books updated?

You risk tax penalties, cash flow issues, inaccurate financial reporting, and potential fraud.

5. What bookkeeping software is best for small businesses?

Popular options include QuickBooks, Xero, FreshBooks, and Wave Accounting.

Final Thoughts

Regular bookkeeping updates are essential for financial accuracy, tax compliance, cash flow management, and fraud prevention. By prioritizing bookkeeping services, businesses can make informed decisions, secure funding, and scale successfully.

If you’re struggling to maintain accurate financial records, consider partnering with a professional bookkeeping service to ensure long-term financial stability and growth.

Need financial guidance?

Consider hiring a fractional Controller to streamline your finances without the cost of a full-time hire.

You might also like these articles

Key Financial Metrics Every Franchisor Owner Should Track

For franchisors, financial management is crucial to sustaining and growing a successful franchise network. With multiple franchisees operating under your brand, keeping a close eye on financial metrics ensures profitability, operational efficiency, and long-term sustainability. This is where franchisor bookkeeping becomes essential. Without accurate financial tracking, franchisors risk cash flow issues, compliance problems, and lost...

Read More

Landscaping Bookkeeping: How to Streamline Your Finances

Running a landscaping business means juggling multiple responsibilities—managing crews, scheduling jobs, maintaining equipment, and, of course, keeping your finances in order. Yet, bookkeeping is often the most overlooked aspect of running a successful landscaping company. Poor financial management can lead to cash flow issues, unpaid invoices, and an inability to make smart business decisions. If...

Read More

9 Benefits of Bookkeeping for Home Service Businesses

Whether you're running a landscaping company, plumbing service, HVAC business, or any other type of home service operation, bookkeeping is one of the most essential—and often underestimated—components of success. While marketing, client satisfaction, and operations are always top of mind, without strong financial practices in place, your business may struggle to grow or stay profitable....

Read More

Introducing Our Exclusive Tax & Advisory Partner: Solutions Group Accounting Firm

At Out of the Box, we’re always looking for ways to deliver more value to our clients—whether that’s providing smarter bookkeeping solutions, scaling with your business needs, or helping you stay ahead of financial complexities. That’s why we’re thrilled to share some exciting news: Out of the Box is now officially partnered with Solutions Group...

Read More

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

March 26, 2025

9 Benefits of Bookkeeping for Home Service Businesses

Whether you’re running a landscaping company, plumbing service, HVAC business, or any other type of home service operation, bookkeeping is one of the most essential—and often underestimated—components of success. While marketing, client satisfaction, and operations are always top of mind, without strong financial practices in place, your business may struggle to grow or stay profitable.

This article explores the top bookkeeping benefits for home service business owners and why it should be a central part of your operations. Whether you’re an entrepreneur just starting out or a seasoned small business owner, understanding how bookkeeping supports your business’s health can save time, reduce stress, and even increase profits.

What Is Bookkeeping and Why Does It Matter for Home Service Businesses?

Bookkeeping is the process of recording and organizing your business’s financial transactions, including income, expenses, payroll, inventory, and more. In home service businesses, this could include:

-

Customer payments for services

-

Vendor invoices for materials or equipment

-

Employee or contractor wages

-

Fuel, vehicle maintenance, and travel expenses

-

Software subscriptions or advertising spend

Accurate bookkeeping ensures that your financial records are current, reliable, and ready for tax time—or for making smart business decisions.

According to the U.S. Bureau of Labor Statistics, approximately 20% of small businesses fail within their first year, and 50% fail within five years. Poor financial management is one of the most common causes. Bookkeeping provides the foundation for sound financial management.

Top Bookkeeping Benefits for Home Service Businesses

1. Improved Cash Flow Management

Cash flow is the lifeblood of any service business. Whether you’re waiting on customer payments or covering payroll, poor cash flow can derail even a profitable company.

With good bookkeeping practices in place:

-

You can track outstanding invoices and follow up with late payers.

-

You’ll know exactly how much money is coming in and going out each week.

-

You can forecast upcoming expenses and prevent cash shortages.

Example: A lawn care company might bill clients monthly but still need to pay employees weekly. With organized books, the owner can spot when they’ll fall short and take action—such as offering early-payment discounts to clients.

2. Easier and More Accurate Tax Preparation

Tax season can be overwhelming, especially if your records are scattered across receipts, spreadsheets, and email chains. Bookkeeping consolidates everything in one place, making tax preparation straightforward.

Benefits include:

-

Accurate expense categorization to ensure you’re claiming all deductions

-

Real-time profit/loss reports to estimate tax liability

-

Easy collaboration with your CPA or tax preparer

According to the IRS, small business owners who keep organized records are less likely to face audits or penalties. Bookkeeping helps reduce errors, lower your tax bill, and avoid compliance issues.

3. Better Business Decision-Making

Without good data, business decisions become guesses. Bookkeeping provides the financial insights you need to:

-

Set pricing based on actual costs

-

Hire new team members at the right time

-

Invest in new tools or marketing strategies

-

Cut wasteful spending

Example: A handyman service reviews their books and finds that advertising on one local platform has a much better ROI than another. By reallocating spend, they increase leads without spending more money.

4. Professionalism and Credibility

Having up-to-date financial records makes you look more credible to banks, investors, and even clients. When applying for a loan or line of credit, you’ll often need:

-

Profit and loss statements

-

Balance sheets

-

Cash flow statements

All of which are made possible through regular bookkeeping.

Additionally, clients who see you operate with professionalism are more likely to trust your services and recommend your business.

5. Simplified Payroll and Contractor Payments

Many home service businesses rely on a mix of full-time employees and independent contractors. Bookkeeping helps you:

-

Track hours and payments accurately

-

Generate paystubs or 1099s for contractors

-

Stay compliant with labor and tax regulations

Example: A cleaning service that pays multiple part-time workers benefits from a clear system that tracks wages, taxes withheld, and reimbursement for supplies or mileage.

6. Tracking Equipment and Supply Costs

From lawnmowers and vans to HVAC tools and plumbing supplies, home service businesses often have significant equipment costs. Bookkeeping helps you:

-

Depreciate assets correctly over time

-

Track maintenance expenses

-

Plan for future replacements

Tip: Using bookkeeping software like QuickBooks can automatically track and categorize these expenses, offering visibility into where your money goes.

7. Compliance and Legal Protection

If you ever face an audit, dispute, or legal review, your books are your first line of defense. Having accurate records protects you in situations involving:

-

Tax audits

-

Employment disputes

-

Vendor disagreements

-

Licensing reviews

Being able to quickly produce financial documentation shows that your business is legitimate and transparent.

8. Scalability and Growth Readiness

Home service businesses often begin as solo operations but grow to include multiple employees, service areas, or even franchise opportunities. Good bookkeeping ensures you’re ready to scale by:

-

Highlighting your most profitable services

-

Tracking margins across different job types

-

Preparing accurate financial projections

Example: A pressure washing business wants to expand into a new neighborhood. Bookkeeping reports show which zip codes generate the most profit, guiding their marketing strategy.

Why QuickBooks is the Best Bookkeeping Tool for Home Service Businesses

At Out of the Box Technology, we recommend QuickBooks as the best-in-class solution for small and home-based service businesses.

Why?

-

It supports double-entry accounting (for more accurate records)

-

It integrates with tools like CRM systems, payment processors, and time tracking apps

-

It offers mobile access, perfect for business owners who are always on the go

-

It provides automated reporting, so you can view your profit & loss anytime

With QuickBooks, tasks like invoice tracking, payroll, mileage logging, and vendor payments become simple. Our team helps business owners with setup, customization, training, and support.

Real-Life Example: From Chaos to Clarity

Meet Susan, who runs a mobile pet grooming business. At first, she tracked income using her PayPal account and stored receipts in a shoebox. By the time tax season rolled around, she had no idea what she owed or what she could deduct.

After partnering with Out of the Box Technology, she started using QuickBooks and set up a bookkeeping system tailored to her business. Within six months:

-

She had clear visibility into her cash flow

-

Her CPA was able to reduce her tax bill by $3,000

-

She confidently applied for a small business loan to buy a second van

Frequently Asked Questions (FAQs)

1. How often should I update my books?

Ideally, you should update your books weekly or at minimum, monthly. This ensures your records are current and helps avoid surprise issues at tax time.

2. Can I do my own bookkeeping or should I hire someone?

Many business owners start by doing their own bookkeeping using tools like QuickBooks. As your business grows, it’s often more efficient and cost-effective to hire a bookkeeping service to ensure accuracy and free up your time.

3. What’s the difference between bookkeeping and accounting?

Bookkeeping involves the day-to-day recording of transactions, while accounting focuses on analyzing and interpreting that data to support decisions, planning, and tax strategy.

4. Is bookkeeping really necessary if I’m a sole proprietor?

Yes. Even if you’re the only person in your business, keeping accurate records protects you from tax issues, helps you understand your business performance, and supports growth.

5. What bookkeeping software do you recommend?

We highly recommend QuickBooks, which offers both simplicity for beginners and robust features for growing businesses. Out of the Box Technology provides full QuickBooks support and integration.

Conclusion: Invest in Bookkeeping, Invest in Your Business

For small business owners and home service entrepreneurs, bookkeeping is more than a back-office task—it’s a strategic asset. From improving cash flow and tax readiness to helping you grow and scale, the benefits are tangible and long-lasting.

Don’t let financial disorganization hold your business back. With the right tools and support, you can turn your numbers into powerful insights that guide better decisions.

At Out of the Box Technology, we help home service businesses implement bookkeeping systems that work. Whether you need help setting up QuickBooks, need monthly support, or are ready to outsource your entire bookkeeping function, we’re here to help.

Ready to take control of your books and boost your business?

Visit www.outoftheboxtechnology.com to learn more about our bookkeeping solutions for home service businesses.

Talk to An Advisor Today

You might also like these articles

Key Financial Metrics Every Franchisor Owner Should Track

For franchisors, financial management is crucial to sustaining and growing a successful franchise network. With multiple franchisees operating under your brand, keeping a close eye on financial metrics ensures profitability, operational efficiency, and long-term sustainability. This is where franchisor bookkeeping becomes essential. Without accurate financial tracking, franchisors risk cash flow issues, compliance problems, and lost...

Read More

Landscaping Bookkeeping: How to Streamline Your Finances

Running a landscaping business means juggling multiple responsibilities—managing crews, scheduling jobs, maintaining equipment, and, of course, keeping your finances in order. Yet, bookkeeping is often the most overlooked aspect of running a successful landscaping company. Poor financial management can lead to cash flow issues, unpaid invoices, and an inability to make smart business decisions. If...

Read More

Introducing Our Exclusive Tax & Advisory Partner: Solutions Group Accounting Firm

At Out of the Box, we’re always looking for ways to deliver more value to our clients—whether that’s providing smarter bookkeeping solutions, scaling with your business needs, or helping you stay ahead of financial complexities. That’s why we’re thrilled to share some exciting news: Out of the Box is now officially partnered with Solutions Group...

Read More

Outsourced Accounting: What It Is and How It Can Benefit Your Home Services Business

Running a home services business—whether it’s landscaping, plumbing, HVAC, roofing, or cleaning services—comes with many moving parts. From managing clients and scheduling jobs to handling employees and equipment, keeping up with financial tasks like bookkeeping and accounting can quickly become overwhelming. That’s where outsourced accounting comes in. Instead of managing your books in-house or struggling...

Read More

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

March 14, 2025

Outsourced Accounting: What It Is and How It Can Benefit Your Home Services Business

Running a home services business—whether it’s landscaping, plumbing, HVAC, roofing, or cleaning services—comes with many moving parts. From managing clients and scheduling jobs to handling employees and equipment, keeping up with financial tasks like bookkeeping and accounting can quickly become overwhelming.

That’s where outsourced accounting comes in. Instead of managing your books in-house or struggling to keep up with QuickBooks on your own, outsourcing your accounting can provide cost savings, expert financial guidance, and greater efficiency—all while letting you focus on growing your business.

In this article, we’ll explore:

- What outsourced accounting is

- How it benefits home services businesses

- Why QuickBooks is the best accounting software for outsourced bookkeeping

- Common accounting challenges in the home services industry

- Frequently asked questions about outsourced accounting

What Is Outsourced Accounting?

Outsourced accounting is when a business hires a third-party accounting firm to handle financial tasks such as:

- Bookkeeping – Recording income, expenses, and transactions

- Accounts Payable & Receivable – Tracking invoices and ensuring payments

- Payroll Processing – Managing wages, employee benefits, and tax filings

- Financial Reporting – Creating reports to track business performance

- Tax Preparation – Ensuring compliance and minimizing tax liability

For home services business owners, outsourcing accounting means less time spent on financial paperwork and more time focusing on running your business efficiently.

Why Home Services Businesses Should Outsource Accounting

1. Save Time & Focus on Growth

Home service providers are always on the go—managing job sites, scheduling crews, and working directly with clients. Outsourcing accounting eliminates the burden of bookkeeping, payroll, and financial reporting, freeing up time to focus on growing your business.

Example: Instead of spending hours reconciling bank statements and chasing late invoices, a landscaping company owner can focus on winning new contracts and improving service quality.

2. Reduce Costs & Increase Profitability

Hiring an in-house accountant can be expensive—salary, benefits, and training all add up. With outsourced accounting, you pay only for the services you need, saving money while ensuring accurate financial management.

Example: A plumbing business that outsources accounting saves over $40,000 per year, money that can be reinvested into tools, marketing, or additional staff.

3. Improve Cash Flow Management

Many home services businesses struggle with cash flow, especially when dealing with seasonal fluctuations or late customer payments. Outsourced accounting helps:

- Track expenses and income accurately

- Send invoices on time and follow up on unpaid accounts

- Monitor cash flow to prevent shortages

Example: A roofing contractor who struggles with delayed client payments uses QuickBooks through an outsourced accountant to automate invoicing and send payment reminders, improving cash flow.

4. Ensure Tax Compliance & Avoid Penalties

Tax laws are complex, and home services businesses must comply with sales tax, payroll tax, and income tax regulations. Outsourced accountants stay up to date with tax laws, ensuring accurate filings and helping you maximize deductions (without mistakes that could trigger an audit).

Example: An HVAC company using QuickBooks with an outsourced accountant saves thousands of dollars by properly classifying business expenses for tax deductions.

5. Access to Financial Insights & Reporting

Outsourced accountants provide detailed financial reports, including:

- Profit & Loss Statements – Understand business performance

- Balance Sheets – Track assets and liabilities

- Cash Flow Reports – Monitor inflows and outflows

With QuickBooks, these reports are generated in real-time, helping home services business owners make smarter decisions about pricing, expenses, and hiring.

Example: A cleaning service owner uses monthly QuickBooks reports to identify peak revenue months and adjust marketing spend accordingly.

Why QuickBooks Is the Best Accounting Solution for Outsourced Accounting

When working with an outsourced bookkeeping service, using the right accounting software is crucial. QuickBooks is the gold standard for home services businesses because it offers:

- Easy Integration with Outsourced Accountants – Share data securely with your accounting team.

- Automated Invoicing & Payments – Reduce late payments and improve cash flow.

- Mobile Access for On-the-Go Business Owners – Manage finances from your phone.

- Job Costing Features – Track profitability by project or client.

- Real-Time Financial Insights – View cash flow, expenses, and profits anytime.

Example: A lawn care business owner uses QuickBooks to track seasonal income, ensuring they budget properly for slower winter months.

For businesses that need fully managed accounting support, Outsourced Bookkeeping and Accounting Services can handle QuickBooks setup, payroll, invoicing, and more.

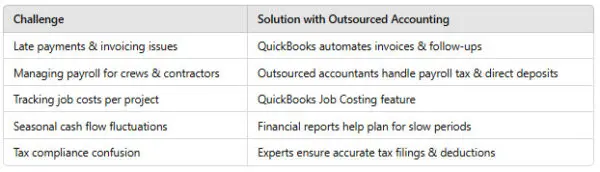

Common Accounting Challenges in Home Services Businesses (And How Outsourced Accounting Solves Them)

FAQs About Outsourced Accounting for Home Services Businesses

1. How much does outsourced accounting cost?

Costs vary based on the level of service needed, but most home services businesses pay between $5,000 – $20,000 per year, which is far less than hiring a full-time accountant.

2. Do I still have control over my finances if I outsource?

Yes. You still make all financial decisions—an outsourced accountant simply manages the numbers and provides insights to help you make informed choices.

3. Can an outsourced accountant help with job costing?

Yes. Job costing is essential for home service businesses. Your accountant will set up QuickBooks Job Costing to track profitability per project.

4. Is QuickBooks the best accounting software for home services businesses?

Absolutely. QuickBooks offers invoicing, payroll, expense tracking, job costing, and mobile access, making it the best choice for home service professionals.

5. How do I get started with outsourced accounting?

You can start by contacting Out of the Box Technology for a customized bookkeeping solution that fits your home services business.

Final Thoughts: Why Outsourced Accounting Is a Smart Move

For home services business owners, outsourced accounting provides time savings, cost efficiency, expert financial management, and peace of mind. Whether you’re running a plumbing, HVAC, roofing, landscaping, or cleaning business, partnering with an outsourced accountant using QuickBooks will help you:

- Reduce financial stress

- Improve cash flow & profitability

- Avoid tax headaches & compliance issues

- Scale your business with confidence

If you’re ready to streamline your bookkeeping and accounting with QuickBooks and expert support, explore Outsourced Bookkeeping and Accounting Services and take the next step toward financial success.

Contact us today to get started!

Talk to An Advisor Today

You might also like these articles

Key Financial Metrics Every Franchisor Owner Should Track

For franchisors, financial management is crucial to sustaining and growing a successful franchise network. With multiple franchisees operating under your brand, keeping a close eye on financial metrics ensures profitability, operational efficiency, and long-term sustainability. This is where franchisor bookkeeping becomes essential. Without accurate financial tracking, franchisors risk cash flow issues, compliance problems, and lost...

Read More

Landscaping Bookkeeping: How to Streamline Your Finances

Running a landscaping business means juggling multiple responsibilities—managing crews, scheduling jobs, maintaining equipment, and, of course, keeping your finances in order. Yet, bookkeeping is often the most overlooked aspect of running a successful landscaping company. Poor financial management can lead to cash flow issues, unpaid invoices, and an inability to make smart business decisions. If...

Read More

9 Benefits of Bookkeeping for Home Service Businesses

Whether you're running a landscaping company, plumbing service, HVAC business, or any other type of home service operation, bookkeeping is one of the most essential—and often underestimated—components of success. While marketing, client satisfaction, and operations are always top of mind, without strong financial practices in place, your business may struggle to grow or stay profitable....

Read More

Introducing Our Exclusive Tax & Advisory Partner: Solutions Group Accounting Firm

At Out of the Box, we’re always looking for ways to deliver more value to our clients—whether that’s providing smarter bookkeeping solutions, scaling with your business needs, or helping you stay ahead of financial complexities. That’s why we’re thrilled to share some exciting news: Out of the Box is now officially partnered with Solutions Group...

Read More

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.

Talk to An Advisor Today

You might also like these articles

The Plumbing Business Owner’s Bookkeeping Playbook

Read More

Running a plumbing business involves far more than just fixing leaks or installing water heaters. As a business owner, you wear many hats—technician, manager, scheduler, and financial decision-maker. But if your bookkeeping isn’t organized and aligned with your day-to-day operations, it can create cash flow problems, compliance issues, and missed growth opportunities. According to the…

Pest Control Bookkeeping 101: A Complete Guide for Owners

Read More

Pest Control Bookkeeping: Essential Tools and Tips for a Thriving Business In the dynamic pest control industry, where mobile technicians, daily invoicing, and strict compliance are the norm, robust bookkeeping is critical for success. This guide is specifically for pest control business owners aiming to streamline finances, guarantee compliance, and utilize financial data for strategic…

Bookkeeping for Big Purchases

Read More

Why Equipment Financing Can Wreck Your Books (If You’re Not Careful) Whether you’re running a landscaping company, HVAC firm, construction outfit, or manufacturing shop, big equipment purchases are inevitable—and expensive. From trucks and trailers to compressors, loaders, and CNC machines, these assets often require financing, multiple vendors, and complex accounting entries. And here’s the catch:…

Job Costing for Contractors: How Better Bookkeeping Improves Profit Margins

Read More

Why Job Costing Is Critical for Contractor Success Contractors face a complex balancing act. Materials, labor, subcontractors, permits, change orders—each project comes with hundreds of moving pieces. But too often, construction business owners find out a job wasn’t profitable only after the final invoice is sent. That’s where job costing makes all the difference. Job…

Claim your complimentary bookeeping assesment today

Request your free bookkeeping quote today and let us simplify your financial management. Our expert team at QuickBooks is ready to tailor a solution to your needs.