For many growing businesses, Microsoft Dynamics (including Dynamics GP, NAV, or Business Central) offers robust ERP features. But as your organization evolves, you may find that the platform becomes too complex or costly for your current needs. That’s when a Microsoft Dynamics migration to QuickBooks becomes an attractive option.

In this guide, we’ll explore when and why a migration makes sense, what the process entails, and how to avoid common pitfalls. If you’re seeking a more cost-effective, user-friendly solution for accounting and financial management, switching to QuickBooks Online or QuickBooks Enterprise might be the right move.

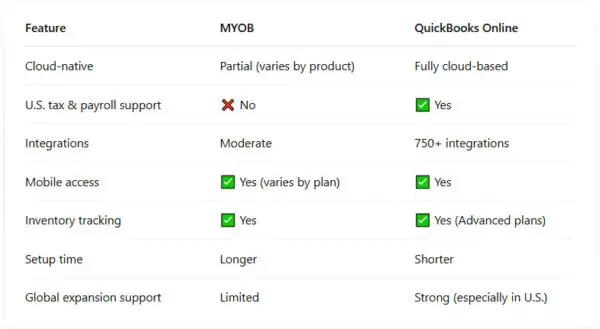

Why Migrate from Microsoft Dynamics to QuickBooks?

While Microsoft Dynamics is powerful, many small and mid-sized businesses are finding that it’s overbuilt for what they need. Let’s look at some of the top reasons organizations are choosing QuickBooks:

1. Lower Total Cost of Ownership

Microsoft Dynamics typically requires more expensive licenses, dedicated servers (on-premise versions), and IT maintenance. QuickBooks Online Advanced starts at ~$200/month for 25 users, significantly reducing overhead costs.

2. Simplified User Experience

QuickBooks is built for non-accountants, whereas Dynamics is more geared toward finance and IT teams. QuickBooks’ intuitive design allows for faster onboarding and less reliance on support teams.

3. Faster Implementation

Implementing or upgrading Dynamics can take months. QuickBooks setup, even including data migration, can often be completed in days or a few short weeks.

4. App Ecosystem & Integrations

QuickBooks integrates with 750+ business apps including Gusto, HubSpot, Shopify, and Stripe—offering strong automation and customization.

5. Cloud-Based Access

QuickBooks Online is 100% cloud-native. While Dynamics 365 is also cloud-based, older versions like GP and NAV are typically on-premise, requiring additional hosting or remote-access workarounds.

Who Benefits from a Microsoft Dynamics Migration to QuickBooks?

A migration to QuickBooks is ideal for:

-

Businesses scaling back from ERP-level complexity

-

Companies with less than 250 employees

-

Service-based businesses, nonprofits, and SMBs

-

Organizations looking to simplify reporting and reduce IT involvement

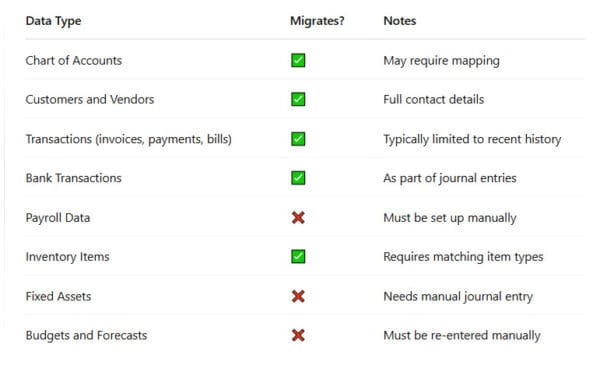

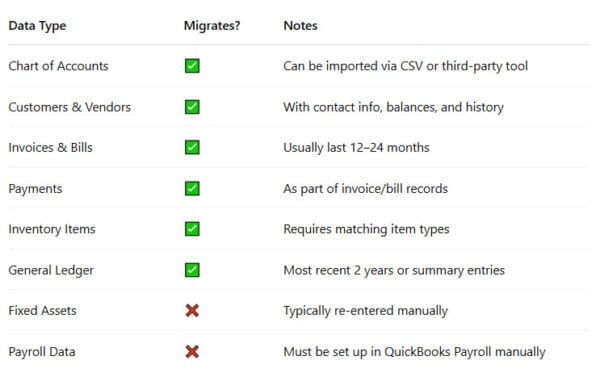

What Data Can Be Migrated from Microsoft Dynamics?

Before migrating, it’s crucial to understand what data can be transferred successfully—and what might need to be recreated in QuickBooks.

Source: Intuit Data Services, SaasAnt Migration Tool

Step-by-Step: How to Complete a Microsoft Dynamics Migration to QuickBooks

Step 1: Evaluate Your Existing Setup

-

Identify Dynamics version (GP, NAV, BC)

-

Inventory current modules in use (AP, AR, Inventory, Payroll)

-

Define which reports and data sets are critical to carry over

Step 2: Choose Your QuickBooks Edition

Most former Dynamics users migrate to:

-

QuickBooks Online Advanced (cloud-based, up to 25 users)

-

QuickBooks Desktop Enterprise (local hosting, extensive reporting)

Step 3: Prepare and Export Your Data

-

Reconcile accounts in Dynamics

-

Export reports for Trial Balance, General Ledger, AP/AR Aging, and Inventory

-

Back up your database for historical records

Step 4: Use a Migration Tool or Partner

Because Dynamics stores data in SQL databases or XML exports, working with a certified migration expert or using tools like Dataswitcher, SaasAnt, or Transaction Pro ensures accurate import and mapping.

Step 5: Import Data to QuickBooks

-

Use QBO’s built-in import for Chart of Accounts, customers, and vendors

-

Import transactions and inventory via CSV or third-party tools

-

Double-check account mapping for consistency

Step 6: Reconcile and Go Live

-

Match balances between systems

-

Test reports (P&L, balance sheet)

-

Set up recurring transactions, bank feeds, and user permissions

Real-World Case Study

Client: B2B Technology Consulting Firm

Problem: Microsoft Dynamics GP required custom development and third-party hosting. Reports took too long to generate and system maintenance costs were high.

Solution: Migrated to QuickBooks Online Advanced with customized reporting and app integrations.

Results:

-

Reduced monthly accounting software spend by 70%

-

Month-end close time dropped from 12 days to 5

-

Improved financial visibility across departments

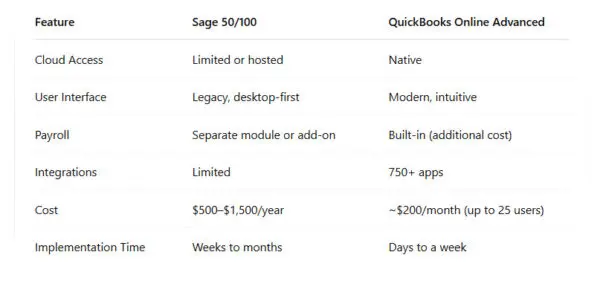

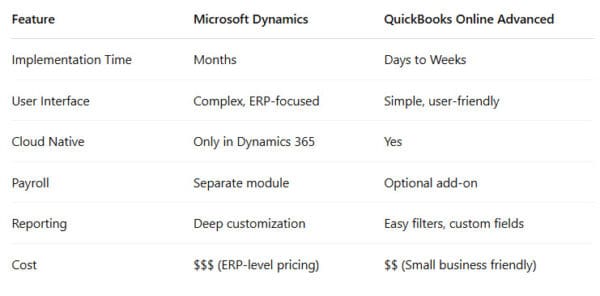

Microsoft Dynamics vs QuickBooks: Feature Comparison

Common Migration Challenges (and How to Solve Them)

1. Chart of Accounts Overload

Dynamics often uses extensive COAs with subcategories. Simplify before import.

2. Data Mapping Errors

Be careful mapping GL accounts, inventory types, and tax settings. Partnering with a ProAdvisor can prevent costly mistakes.

3. Large Historical Data Volumes

Limit import to 1–2 years of detail. Archive the rest and post journal entries for historical balances.

4. Integrations Loss

Not all third-party integrations transfer. You’ll need to rebuild connections in QuickBooks using Zapier or direct APIs.

FAQs About Microsoft Dynamics Migration to QuickBooks

Q: Can I migrate from Microsoft Dynamics GP to QuickBooks Online?

A: Yes, though GP stores data in SQL databases, requiring conversion to CSV or use of migration tools.

Q: Will I lose historical data?

A: Not necessarily. You can import summaries or 1–2 years of transaction history. Archive the rest as PDFs or backups.

Q: Is QuickBooks secure for sensitive financial data?

A: Yes. QBO uses 128-bit SSL encryption and is hosted on SOC 2-compliant infrastructure.

Q: Can I get help from Intuit for this migration?

A: Intuit’s data migration team offers limited support, so for Dynamics, it’s best to use a certified partner or tool.

Q: Can I run both systems in parallel during transition?

A: Yes, but ensure strict cut-off dates and reconciliation to avoid double-entry or conflicting records.

Final Thoughts

A Microsoft Dynamics migration to QuickBooks is a strategic decision for companies that want agility, lower costs, and an easier accounting experience. With careful planning and the right tools, you can move from enterprise-grade ERP to a nimble, cloud-based system—without losing essential data or insights.

Whether you’re using Microsoft Dynamics GP, NAV, or Business Central, our team of certified ProAdvisors can help you plan and execute a smooth migration tailored to your business.

Need Expert Help Migrating from Dynamics to QuickBooks?

We specialize in complex accounting system migrations. Let us handle the details while you focus on your business.

Schedule your free migration consultation today.