When it comes to accounting methods, businesses have two primary choices: cash basis accounting and accrual basis accounting. The choice between these methods affects financial reporting, tax liabilities, and overall business strategy.

This article will explain the differences between cash and accrual accounting, outline their advantages and disadvantages, provide real-world examples, and discuss best practices for choosing the right method for your business.

What is Cash Basis Accounting?

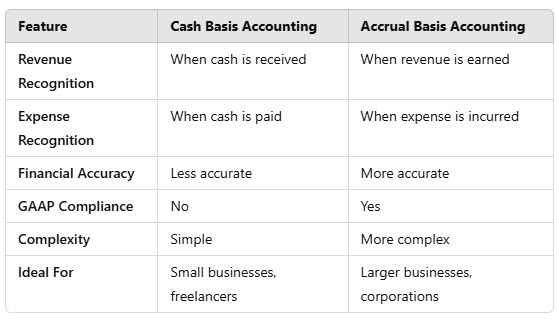

Cash basis accounting is a straightforward method where transactions are recorded when cash is received or paid. This means revenue is recognized only when the business receives payment, and expenses are recorded when they are paid out.

Key Features:

- Revenue is recognized only when cash is received.

- Expenses are recognized only when cash is paid.

- No accounts receivable or accounts payable.

- Provides a clear picture of available cash.

Example of Cash Basis Accounting:

Imagine a freelance graphic designer completes a project in December but receives payment in January. Under cash basis accounting, the income is recorded in January, when the payment is received, rather than December, when the work was completed.

Advantages of Cash Basis Accounting:

- Simple and easy to manage – Ideal for small businesses and sole proprietors.

- Reflects actual cash flow – Since revenue and expenses are recorded only when cash changes hands, it shows available cash at any given moment.

- Tax advantages – Businesses can defer income by delaying invoice payments until the next tax year.

Disadvantages of Cash Basis Accounting:

- Doesn’t show true profitability – Since revenue and expenses aren’t matched to when they occur, profitability can appear misleading.

- Not GAAP-compliant – Public companies and larger businesses must use accrual accounting under Generally Accepted Accounting Principles (GAAP).

- Limited financial insight – With no accounts receivable or payable, financial statements may not accurately represent business obligations.

What is Accrual Basis Accounting?

Accrual basis accounting records revenue and expenses when they are earned or incurred, regardless of when cash is received or paid. This provides a more accurate representation of a business’s financial position.

Key Features:

- Revenue is recorded when earned, even if cash isn’t received.

- Expenses are recorded when incurred, even if they aren’t paid immediately.

- Uses accounts receivable and accounts payable.

- Required for businesses that exceed $25 million in annual revenue (as per IRS rules).

Example of Accrual Basis Accounting:

A construction company completes a project in December but receives payment in January. Under accrual accounting, the revenue is recorded in December, when the work was done, rather than when the payment is received.

Advantages of Accrual Basis Accounting:

- Provides a more accurate financial picture – Revenue and expenses are matched to the period they relate to.

- GAAP-compliant – Required for publicly traded companies and large businesses.

- Better long-term financial planning – Helps businesses assess profitability and plan for future expenses.

Disadvantages of Accrual Basis Accounting:

- More complex – Requires tracking accounts receivable, accounts payable, and other accruals.

- Can create cash flow issues – A business may appear profitable on paper while lacking actual cash.

- Higher accounting costs – Requires more sophisticated bookkeeping and financial oversight.

Key Differences Between Cash and Accrual Basis Accounting

Best Practices for Choosing the Right Accounting Method

Best Practices for Choosing the Right Accounting Method

When to Use Cash Basis Accounting:

- If you’re a small business or freelancer – Cash basis is easier to manage.

- If you want simplicity – Less record-keeping and fewer accounting complexities.

- If tax deferral benefits you – Helps manage taxable income by controlling when revenue is recognized.

When to Use Accrual Basis Accounting:

- If your business earns over $25 million annually – The IRS mandates accrual accounting.

- If you need a full financial picture – Helps with long-term planning and decision-making.

- If you deal with inventory – Required under GAAP and IRS rules for inventory-heavy businesses.

Hybrid Accounting Approach:

Some businesses use a hybrid approach, combining elements of both cash and accrual accounting. For example, they might use cash basis for taxes but accrual for internal financial reporting.

Data and Statistics on Accounting Methods

According to a 2022 QuickBooks survey:

- 67% of small businesses in the U.S. use cash basis accounting.

- 100% of Fortune 500 companies use accrual accounting, as required by GAAP.

- Businesses that switch from cash to accrual see an average 22% improvement in financial forecasting accuracy.

Frequently Asked Questions (FAQs)

1. Is cash basis accounting allowed for tax purposes?

Yes, businesses with less than $25 million in revenue can use cash basis accounting for tax reporting.

2. Can I switch from cash to accrual accounting?

Yes, but you must file Form 3115 (Application for Change in Accounting Method) with the IRS.

3. What type of businesses must use accrual accounting?

Businesses that:

- Earn more than $25 million in revenue.

- Sell inventory.

- Are publicly traded or follow GAAP.

4. Why does the IRS prefer accrual accounting?

Accrual accounting provides a more accurate representation of taxable income, reducing the potential for tax manipulation.

5. Which method is better for startups?

Startups often start with cash basis accounting for simplicity but may transition to accrual basis as they grow.

Conclusion

Choosing between cash basis vs. accrual basis accounting depends on your business size, complexity, and financial needs. While cash basis accounting is simpler and helps manage cash flow, accrual accounting offers a clearer picture of long-term profitability and is required for larger businesses.

If you’re unsure which method to choose, consulting with a bookkeeping professional can help you determine the best approach for your business. Regardless of your choice, maintaining accurate financial records is key to long-term success.