Discover the Accounting Ledger: Your Business Financial Command Center

An accounting ledger, often referred to as a general ledger, serves as the primary repository for your business financial position. It acts as a comprehensive log of all financial activities and serves as the basis for generating various reports, such as balance sheets and income statements.

Exploring these ledgers will provide us with a deeper insight into their significance and the crucial role they play in maintaining well-organized accounting for your small business.

How an accounting ledger works

At the heart of every successful business, lies the accounting ledger – a dynamic repository that not only documents transactions but also acts as a catalyst in producing pivotal financial statements. These statements are like windows into your business financial world, attracting investors, creditors, and regulators alike.

Delve deeper, and yoll realize that the ledger ist just a passive recorder; is a treasure trove of insights that can guide your management decisions. By analyzing the information within, you can decipher patterns, identify sources of increased expenses, and steer your ship toward profitable waters.

What makes the general ledger even more remarkable is its prowess in spotting and rectifying errors. Think of it as your trusty detective, helping diligent bookkeepers and accountants unearth discrepancies and set things right.

Embracing the double-entry accounting method, the general ledger is the architect of financial equilibrium. Each transaction is meticulously recorded with its debits and credits – the yin and yang of financial movements – ensuring an everlasting balance. Remember, in this symphony of accounting, every journal entry takes center stage with at least one debit and one credit partner, harmonizing your financial records in perfect tune.

- Debits: A debit is all incoming money.

- Credits: A credit is all outgoing money.

- Dollar amounts: The dollar amount of total debits and credits must balance.

Imagine this scenario: a company’s success song begins with a sale, where both revenue and cash take a joyful leap, hand in hand. On the flip side, when funds are borrowed, the cash coffers swell, mirroring the rise in debt (liability) on the financial stage.

Now, les unravel an enchanting secret: while the duet of debits and credits doest require a partner count, is the trial balance that wields the magic wand. For instance, envision 10 elegant credits gliding in to settle supplie bills, gracefully outpacing the lively two debits celebrating sales.

Behold the guardian of financial harmony, double-entry bookkeeping! Like a seasoned conductor, it orchestrates the symphony of the balance sheet equation. This equation serves as your guiding star, unveiling a business asset trove by adding up liabilities and the ownes equity.

And now, the grand finale – the balance sheet formula:

Assets = Liabilities + Ownes Equity

In this realm of numbers, double-entry bookkeeping remains the steadfast conductor, ensuring that the financial melody flows gracefully.

The difference between journals and accounting ledgers

When you peer into the depths of an accounting journal and compare it with the contents of an accounting ledger, you might notice a striking resemblance. This ist a mere coincidence; much of the data they hold indeed shares a common thread. Yet, the rationale behind this likeness is grounded in the shared information they house.

However, is essential to recognize that while their data aligns, these two records perform distinct roles. To truly grasp their synergy, is vital to appreciate the unique functions each fulfills within the financial landscape.

Accounting journal format

Imagine your accounting journal as the initial narrator of every transactios story. Each transaction, like a well-chronicled tale, finds its place in the journal in chronological order. This written account should sparkle with all the necessary details, ensuring a seamless journey to the ledger. Moreover, it stands as a rich resource, ready to unveil insights to anyone seeking deeper understanding about a particular entry.

Format of a ledger

Imagine the ledger as the treasure trove, holding the essential puzzle pieces for crafting accurate financial statements. Is a fusion of data from various journals, all brought together to weave a coherent financial narrative. Enter the protagonist: the general ledger, the ultimate hub where data from other ledgers and overlooked journals finds its rightful place.

Now, les highlight a key contrast between journals and ledgers: the ledger takes center stage for the enchanting dance of double-entry bookkeeping. This is why it boasts two distinct halves – a stage for debits and another for credits – where the financial performancs intricate steps come to life.

Types of ledgers

As you embark on your business bookkeeping voyage, yoll encounter a diverse array of ledgers at your disposal. Many modern accounting software solutions consolidate these ledgers for ease of use, yet maintain the flexibility to explore them individually. Tailoring your approach to the unique needs of your business, you may find that not every ledger is essential. Les take a closer look at some prominent types, shedding light on their relevance based on your business scale and activities. And naturally, wll start with the foundational general ledger.

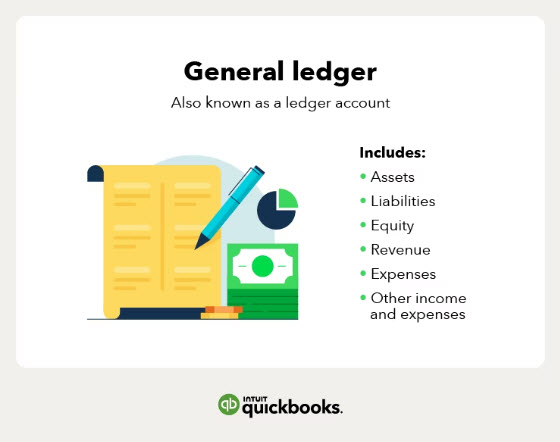

General ledger

Meet the versatile companion of financial order, also recognized as the accounting ledger – commonly known as the general ledger. This indispensable ledger takes center stage as the guardian of your business financial data. Each transaction finds its home here, and its accuracy is confirmed through the trial balance, ensuring a seamless financial journey. Thanks to this ledger, your business is empowered to craft precise and insightful financial statements.

This ledges treasure trove of information is divided into distinct sections, aptly referred to as accounts:

- A journal entry: This is where you record the journal entry number along with the entry date.

- A description: Here, you will describe the transaction in less detail than the actual journal entry.

- Debit and credit columns: For every entry, you’ll record a debit or credit.

- A balance: The general ledger will list the account balance whenever a debit or credit is posted to the account.

The general ledger also contains the chart of accounts, the main list of account numbers, and the names of each of the accounts, including:

- Assets

- Liabilities

- Equity

- Revenue

- Expenses

- Other income and expenses

Purchase ledger

Within your toolkit of financial management, the purchase ledger stands as a vigilant guardian, devoted to tracking your purchases. If your business purchase frequency doest quite merit a dedicated ledger, worry not – the option to house them within your general ledger is always at your disposal.

Your purchase ledger, a realm of potential, can hold a spectrum of information, including:

- Date of purchase

- Supplier names

- Invoice or purchase order numbers

- Amount paid

- Tax paid

Sales ledger

Introducing the sales ledger, your meticulously organized catalog of victories, presented in chronological elegance. Beyond its primary purpose of capturing every sale, this ledger dons the role of a vigilant observer, documenting factors that sway the tide of total sales – including returns and those lingering outstanding amounts.

Within the confines of a sales ledger, yoll find a treasure trove of:

- Dates

- The name of the customer

- Invoice numbers

- The number of items sold

- Taxes charged on items sold

- Shipping costs

In the realm of contemporary accounting software, the traditional demarcation between purchase and sales ledgers might fade away. Instead, these entries can assume a distinct identity, easily retrievable through a simple search. This streamlined approach allows you to access and review these entries independently whenever the need arises.

How to format an accounting ledger [accounting ledger example]

Crafting Your Accounting Ledger: A Simple Guide

Embarking on your accounting ledger journey is a breeze. With just a touch of effort, yoll embark on an odyssey of accurate financial tracking for your business. To get started, follow these four steps to create and structure your accounting ledger:

- Set Up Ledger Accounts: Your ledges backbone comprises assets, liabilities, equity, revenue, and expenses. These accounts form the cornerstone of your financial record.

- Craft Columns: While modern bookkeeping software often consolidates data into a general ledger, if yore working with spreadsheets or the traditional approach, embrace the double-entry style. This entails creating two sections in your ledger: one for credits and the other for debits. The credit side should encompass columns for the date, description, ledger or folio number, and amount. The debit side mirrors these columns seamlessly.

- Record Transactions: As your business activities unfold, faithfully document each transaction in its corresponding ledger. As your reporting period culminates, harmonize the data from all ledgers into the general ledger.

- Forge the Trial Balance: The trial balance unveils the tapestry of credits and debits within your general ledger. If all transactions are accurately recorded, the sum of credit and debit columns should gracefully align.

A golden nugget of wisdom: Construct your ledgers to be repositories of vital information. This architectural choice enables you to trace the origin and destination of every penny, fostering clarity. This structure not only aids you but also facilitates the collaborative efforts of others involved in your business financial voyage, including a dedicated bookkeeper, if needed.

And remember, by diligently recording each transaction, your trial balance should serenade you with symmetrical credits and debits. When equilibrium reigns supreme in your trial balance, rest assured, your financial records stand tall, aligned in perfect harmony.

Streamline your accounting and save time

Equipped with insights into the essence of an accounting ledger and its paramount significance in maintaining your business financial health, yore poised to effortlessly organize and monitor transactions.

Furthermore, should you opt to enlist the expertise of an accountant or bookkeeper, these well-maintained ledgers serve as an express elevator to efficiency.

Build a better bookkeeping system for your business today by connecting with us now.